Bitcoin SV Surge: Key Drivers & Market Impacts

.jpg)

Market Outlook

The crypto asset market has seen some remarkable gains over the last two weeks, with this week representing a consolidation of prices as Bitcoin (BTC) briefly brushed past the $9,000 mark on Sunday 19 January. Unexpectedly, the best performer over this period has been Bitcoin SV (BSV) — a fork of Bitcoin Cash which was, in turn, a fork of Bitcoin — which numerous analysts have commented on with their own theories as to the reason. So the question remains: What caused the Bitcoin SV price spike?

The chart below shows Bitcoin SV's performance since the start of the year where the asset has returned about 218%, in just three weeks.

It's likely that Bitcoin SV's price surge may have been facilitated by the fact that, as a fork of a fork, it is likely that many BSV holders either no longer have access to their holdings or simply never claimed them — moreover, newly-minted BSV created since its fork in November 2018 are likely to have accrued to only a few entities given its likely lack of mining competition. One data point which suggests this is the relatively little competition among mining pools for Bitcoin SV compared to Bitcoin as we show below — it is likely the 'unknown' segments in both cases represent other large mining entities for the most part.

There is evidence to suggest that recent price movements could have been driven primarily by entities who had received mining rewards since the fork, rather than by organic demand from new BSV investors. Thanks to the open nature of blockchains we can estimate the average time investors hold BTC or BSV before they then transact with it again — whether to buy a good, transfer holdings to a new wallet, or sell the asset. Whilst not a perfect measure, this metric — typically called "Dormancy" — is useful in understanding the holding habits of investors for an asset like BSV.

BSV's dormancy statistic is noticeably higher than BTC's, at around 13 days compared to 8 days for BTC. All things being equal, the higher the dormancy the older coins are being transacted on that day for BSV than BTC, which in turn means that longer-term investors of BSV are releasing their coins into circulation at a higher rate than that of BTC currently. This is especially noticeable, as previously mentioned, due to the fact that many of the oldest holders of BSV — those who held BTC before the fork in November 2018 — may not even have access to the asset anymore, or if they did will have likely sold their holdings by now.

Given the nature of BSV's price surge likely being driven by longer-term investors (such as miners), it is unlikely its performance is sustainable in the following months. We expect BSV to be subject to noticeable volatility over the coming weeks as it eventually returns to pre-2020 levels.

The performance of the top five crypto assets is a follows — BTC (-2.20%), ETH (0.53%), XRP (-0.95%), BCH (-2.08%), and LTC (-2.80%).

Average adjusted transaction volumes continued their week-on-week rise from an average daily total of $2.07B to $2.76B — BTC ($2.10B), ETH ($283M), XRP ($115M), BCH ($214M), and LTC ($45.8M).

Podcast - Reviewing the Top Crypto Predictions of 2020

In this episode, the 21Shares team came together to review the top crypto predictions and theses of 2020 from Coinbase, Messari, and Blockchain Capital. The main predictions that the 21Shares team review in this episode are: (1) that the number and size of mergers and acquisition activity will increase in the years to come; (2) that general use of blockchain technology will become common; and (3) that the market capitalization of stablecoins will continue to grow rapidly.

Have a listen to our first episode of the year!

Reading Materials: Messari's Crypto Theses for 2020; Blockchain Capital’s 2019 Year in Review; Brian Armstrong's (Coinbase) "What will happen to cryptocurrency in the 2020s" blog

Listen on Megaphone, Spotify, or Apple Podcasts.

News - Regulated Derivatives Will ‘Legitimize’ Crypto, Says CFTC Chair | The Block

What happened?

Christopher Giancarlo, the former chairman of the Commodity Futures Exchange Commission (CFTC), has created a nonprofit to promote the idea of digitizing the U.S. dollar. According to a press release shared with The Block on Thursday, the nonprofit, the Digital Dollar Foundation, will study converting the dollar into a blockchain-based digital currency.

IT giant Accenture is supporting “crypto dad” Giancarlo’s foundation. Accenture has been working with a number of central banks on digital currencies, including the Bank of Canada, the Monetary Authority of Singapore, the European Central Bank, and Sweden's Riksbank. The nonprofit’s other founders are Daniel Gorfine, a former CFTC official, and Giancarlo’s brother Charles Giancarlo, a former executive at both Cisco Systems and private-equity firm Silver Lake Partners.

Why does this matter?

As pointed out by our team in the latest episode of our podcast, the stablecoin market's main driver of mainstream interest over the coming year is likely to be from central bank digital currency (CBDC) efforts from the likes of China and, now, U.S. institutions.

Christopher Giancarlo is well-known within the crypto asset industry for his optimism on the potential of the technology whilst he was at the CFTC. The launch of his foundation to promote dollar-based CBDC efforts is undeniably a reaction to the efforts coming from China, as well as perhaps fears over Facebook's Libra. Despite the interest from industry heavyweights, this is perhaps also a sign that any viable CBDC project from the United States and its federal reserve are unlikely to happen any time soon.

Learn more here.

News - Regulated Derivatives Will ‘Legitimize’ Crypto, Says CFTC Chair | CoinDesk

What happened?

Chair Heath Tarbert told Cheddar on Monday his agency is helping create a regulated futures market investors would be able to "rely on" for better "price discovery, hedging and risk management."

"By allowing [cryptocurrencies] to come into the world of the CFTC," investors can better access trusted and regulated financial products, improving overall confidence in the asset class, according to Tarbert. "It's helping to legitimize [digital assets], in my view, and add liquidity to these markets."

When asked by Cheddar whether any other cryptocurrencies, such as XRP, could soon be defined as commodities, Tarbert told investors "to watch this space" as the CFTC works closely with the SEC to "really think about which [crypto] falls in what box."

Why does this matter?

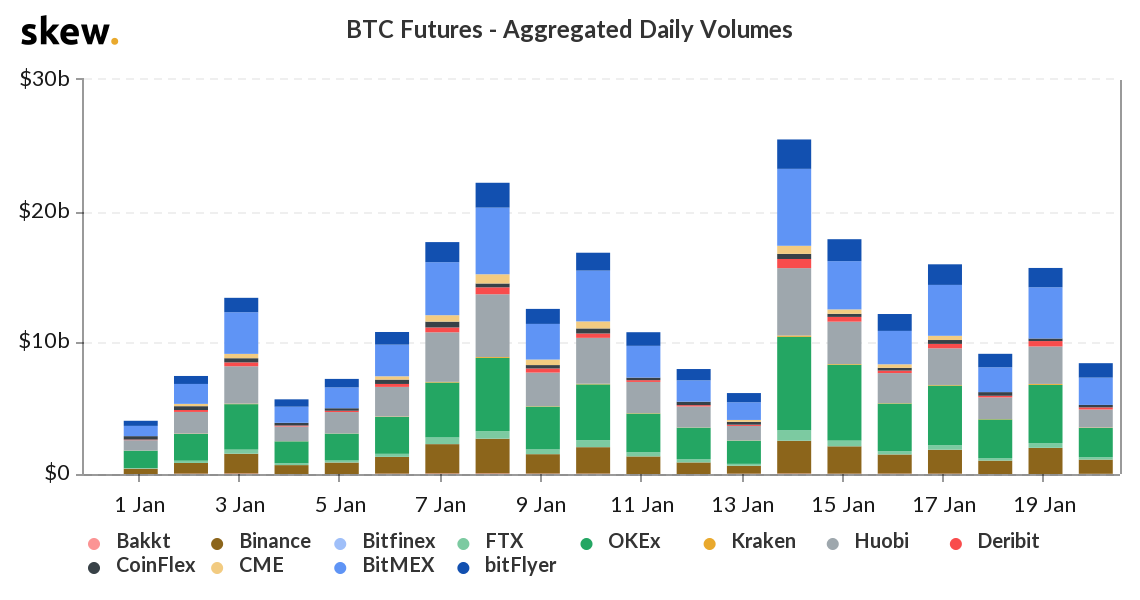

One of the growing narratives we've seen already within 2020 has been the importance of the crypto derivatives market within the wider crypto microstructure. As mentioned last week, we've already had the launch of several Bitcoin options contracts already this year — which should help further support Chair Heath Tarbert argument.

One thing to note however is that, as of now, the unregulated crypto derivatives market currently is drastically larger than its regulated counterpart (in the form of Bakkt's and CME's Bitcoin futures and options). It is likely that both issuers will struggle to capture a sizeable amount of the volume currently within the unregulated market without regulatory crackdowns or changes in compliance strategy from exchanges like BitMEX and Binance.

The chart below shows Bitcoin futures volume over the last six months. As we can see, both CME and Bakkt's Bitcoin futures volume is dwarfed by the products of several crypto-native exchanges.

Learn more here.

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction.

Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.

The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.