Crypto Market Dip & Tether Manipulation: Key Updates

.jpg)

Market Outlook

Over the last week, Bitcoin once again dipped below $9,000 with the rest of the top crypto assets also performing badly — BTC (-7.49%), ETH (-0.868%), XRP (-8.52%), BCH (-1.82%), and LTC (0.397%).

Adjusted transaction volumes fell drastically throughout the week, mirroring the downturn in crypto asset returns — BTC ($2.09B), ETH ($233M), XRP ($152M), BCH ($114M), and LTC ($41M).

Research - A Brief Analysis of the Tether-Bitcoin Market Manipulation Accusation

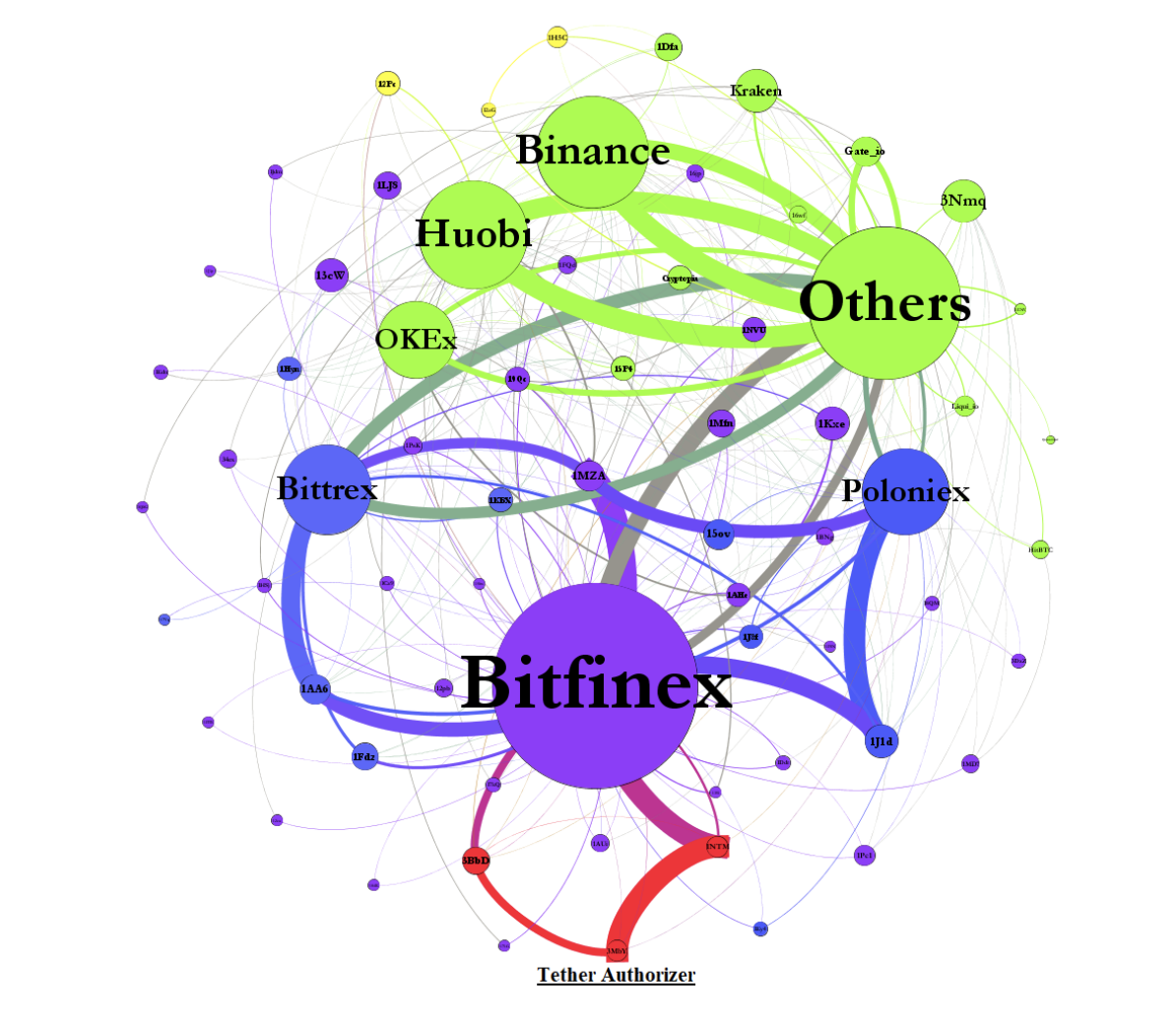

Last week we discussed the news of the release of the updated research paper entitled "Is Bitcoin Really Un-Tethered?" by John M. Griffin and Amin Shams which alleged that the Bitcoin and the wider crypto asset market had been manipulated by a single entity through the printing of tether throughout the bull market of 2017.

As we mentioned last week, the paper was met by scepticism by many in the industry and Tether themselves have since come out to criticise and deny the findings of the report.

Given its length, it's likely that very few in the industry have actually taken the time to read the paper in length but our research team has. The main argument of the paper is as follows:

There are two plausible arguments for the relationship between tether issuance and Bitcoin price returns — the demand-driven hypothesis and the supply-driven hypothesis

The demand-driven hypothesis is where "Tether is driven by legitimate demand from investors who use Tether as a medium of exchange to enter their fiat capital into the crypto space because it is [a] digital currency with the stability of the dollar ‘peg.’ In this case, the price impact of Tether reflects natural market demand."

The supply-driven hypothesis is where "Bitfinex prints Tether regardless of the demand from cash investors. In this case, additional supply of Tether can create ... inflation in [the] price of Bitcoin that is not from a genuine capital flow."

Griffin and Shams use several heuristics to argue for the supply-driven hypothesis as opposed to the demand-driven hypothesis: the timing of the issuances of tether and increases in Bitcoin prices, Bitcoin address clustering to ostensibly discern that a single entity is behind the manipulation, strongly negative end-of-month returns during months when tether is issued, and clusters of Bitcoin purchases around round numbers on Bitfinex during months of tether issuance

As Elaine Ou pointed out in her article for Bloomberg, the authors of the paper draw too strong conclusions from the data they have. For example, the authors make the argument that, on days of tether issuance, the flows of capital from tether to Bitcoin significantly increases around round price thresholds — to suggest that a single entity is attempting to prop the price of Bitcoin up by relying on the cognitive biases of traders. A much simpler argument would be that, as the authors mention but dismiss, that accounts associated with Bitfinex and tether wallets — whether they be Bitfinex-based market makers or "whales" who use Bitfinex — are also subject to biases to round numbers.

In addition, the evidence to suggest that the behaviour described in the paper was driven by a single entity — dubbed "1LSg" — is inconclusive as the paper doesn't consider the possibility that the address in question is simply used as a custodial address, representing the funds of many individual users on Bitfinex — a common practice for crypto asset exchanges.

The difficulty with such analysis is that it is almost impossible to conclusively prove such a case of market manipulation without data on tether and Bitfinex's internal books as well as data from their various payment providers — it was this kind of detail which allowed researchers to uncover evidence suggesting that Bitcoin's price was manipulated on Mt. Gox in 2014.

Our research team will keep abreast of further developments in stories around Tether and Bitfinex so stay glued to our weekly research newsletter!

Podcast - Consumable Digital Commodities

In this week's episode, the 21Shares team is joined by Dr. Stephen McKeon (Partner at Collaborative Fund) to discuss the emergence of digital commodities and how blockchain technology is used to democratize these new types of commodities which were previously exclusively supplied by large centralized entities.

From the 21Shares team, the participants are Ophelia Snyder, Hany Rashwan and Greg Shaheen. This podcast is presented by BlockWorks Group. You can listen to the episode on Spotify or Apple Podcasts.

News - Bakkt Expands Bitcoin Custody Service Beyond Futures Trading Clients | CoinDesk

What Happened?

Bakkt is ready to store customers’ Bitcoin. Intercontinental Exchange’s bitcoin subsidiary announced on Monday it would provide custody services for institutional clients. Pantera Capital, Galaxy Digital and Tagomi have already signed on as initial customers for the “Baakt Warehouse,” with other “marquee firms” expected to join over the next few weeks.

When it first launched, Bakkt was only able to provide custody services to clients trading its bitcoin futures contracts. Monday’s news comes amid an additional approval by the New York Department of Financial Services (NYDFS), which previously granted the company a trust charter.

In a blog post, Bakkt COO Adam White wrote that “a critical link … in the institutional adoption of bitcoin is custody ... [w]hen investors have ready access to regulated custodians whose security and processes they trust, the full potential of this emerging asset class and technology can flourish.”

Why Does This Matter?

We have talked in a previous edition of the newsletter about how Bakkt's custodial solution would likely be just as an important product as its physically-settled futures contracts. As such, Bakkt's move to swiftly open up their custodial solution to the wider public, outside of those who are just trading their futures contracts, is an obvious move.

The crypto custody space is extremely competitive with long-running incumbents like BitGo, Kingdom Trust, and Xapo, as well as newer entries such as Coinbase Custody, Anchorage, and Fidelity Assets. However, despite this Bakkt has a unique selling point given the easy access the Bakkt Warehouse offers to Bakkt's futures trading facilities and the firm's close ties to its parent, the Intercontinental Exchange (ICE).

Learn more here.

News - Bitmain’s Ousted Co-founder Micree Zhan Says He Will Take Legal Action to Return to the Firm | The Block

What Happened?

Micree Zhan, co-founder of crypto asset mining giant Bitmain, was abruptly ousted from the company last week. Zhan now says that he is going to take legal action to return to the firm. In an open letter posted on his WeChat account on Thursday, Zhan said that he was removed from the company without his consent while he was on a “business trip.”

Zhan assured Bitmain staff and shareholders that he will “return to the company as soon as possible through legal methods” to achieve business goals.

Why Does This Matter?

This announcement from Zhan follows news last week (which we covered in last week's newsletter) of the letter that Bitmain co-founder Jihan Wu sent to employees saying that he had taken over Zhan's responsibilities. It remains to be seen what the outcome of such legal proceedings is likely to be, but if Zhan's account of his ousting is accurate one can imagine that he has a relatively strong case.

It is interesting to note that Jihan Wu is still running his new company, Matrix, alongside his recently-claimed duties at Bitmain — we can imagine that issues at Bitmain may slightly impact Wu's plans for his new OTC platform.

Learn more here.

News - Coinbase Will Now Reward Users for Holding XTZ | CoinDesk

What Happened?

Coinbase is for the first time allowing general users to earn rewards by simply holding crypto assets, starting with the Tezos (XTZ) token.

In a company blog published last Wednesday, Coinbase said U.S. customers (barring residents of Hawaii and New York) can now stake the smart-contract platform’s crypto with an estimated 5 percent annual return.

Why Does This Matter?

Coinbase adding the ability for all of its customers to benefit from the additional XTZ generated through staking follows similar moves by its key competitor, Binance. We at 21Shares are excited by the potential staking has to help investors in our ETPs generate returns and will be announcing a first-of-its-kind staking product soon — stay tuned to our social media to be the first to learn more. The chart below plots staking and lending yields across the most popular crypto assets with data from Staked.

Learn more here.

Disclaimer

The information provided does not constitute a prospectus or other offering material and does not contain or constitute an offer to sell or a solicitation of any offer to buy securities in any jurisdiction.

Some of the information published herein may contain forward-looking statements. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties and that actual results may differ materially from those in the forward-looking statements as a result of various factors.

The information contained herein may not be considered as economic, legal, tax or other advice and users are cautioned to base investment decisions or other decisions solely on the content hereof.